I freelanced for some time during the Fall of 2020 and my past work helped me land a 3-month contract with a multinational personal finance company (think WalletHub, NerdWallet etc.).

The client had a credit monitoring app that would help you track your credit score, total debt, insurance money etc.

The insights generated from these were very limited and the client wished to explore the idea of introducing a personal money management app to their existing line of products.

The goal was to track consumers' saving and spending habits to generate more actionable insights that'd help them get to their financial goals faster.

Analytics showed 73% of the client's user base were millenials (born between 1980-2000). And since my research goal was more exploratory than conclusion-driven, I surfaced the idea to restrict the research audience to just millenials, to the client. We were in agreement.

The client's existing product line was mobile-only but they were open to the idea of exploring other messaging channels to communicate with their customers.

Note:There are some administrative hoops one has to jump across, before collecting users' data, in-app or otherwise. Having owned a credit-monitoring app, the client had already gained approval for some of it and asked me to assume the rest would eventually be granted, for the project, should we move forward with a money management app.

I interviewed 8 people, (5 men, 3 women, 2 of whom were students and 5, early career professionals) and asked them questions related to their money management behaviors.

Students include anyone pursuing a full-time undergraduate or graduate degree and they may or may not have a part-time job. Working professionals include people having a full-time job and they may or may not be pursuing a degree.

The findings derived from these were, to a large extent, influenced by the person's economic background, culture and family upbringing.

There were some common themes between responses from savers and spenders -

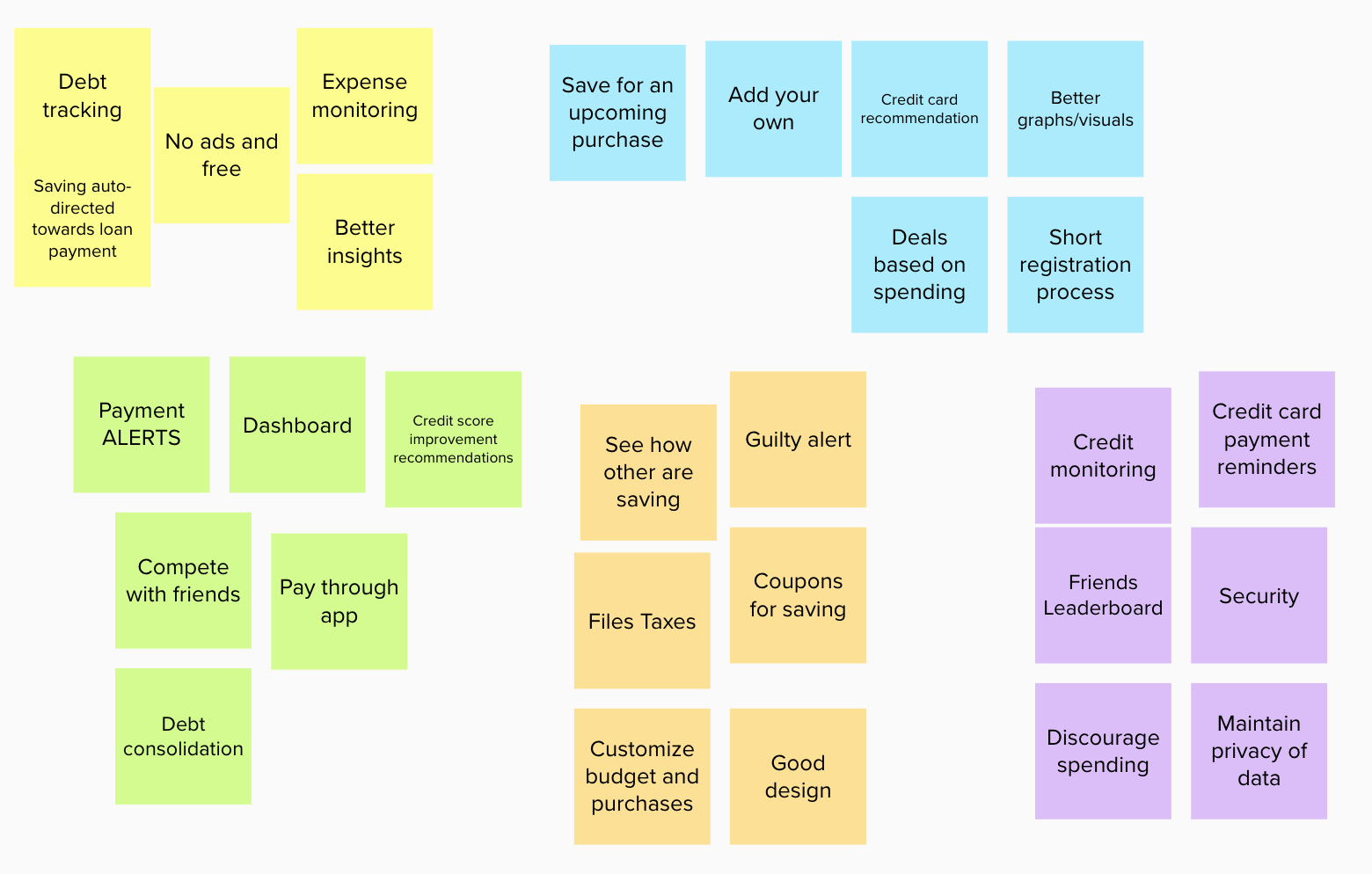

I invited my participants for a group dot-voting exercise using Mural. We followed a divergent-convergent brainstorming technique where we initially thought of all possible ideas a money-management app could have and then converged on a few for the minimum-viable product (MVP).

The shortlisted categories were then used in a closed card sorting exercise to develop the information architecture of the application.

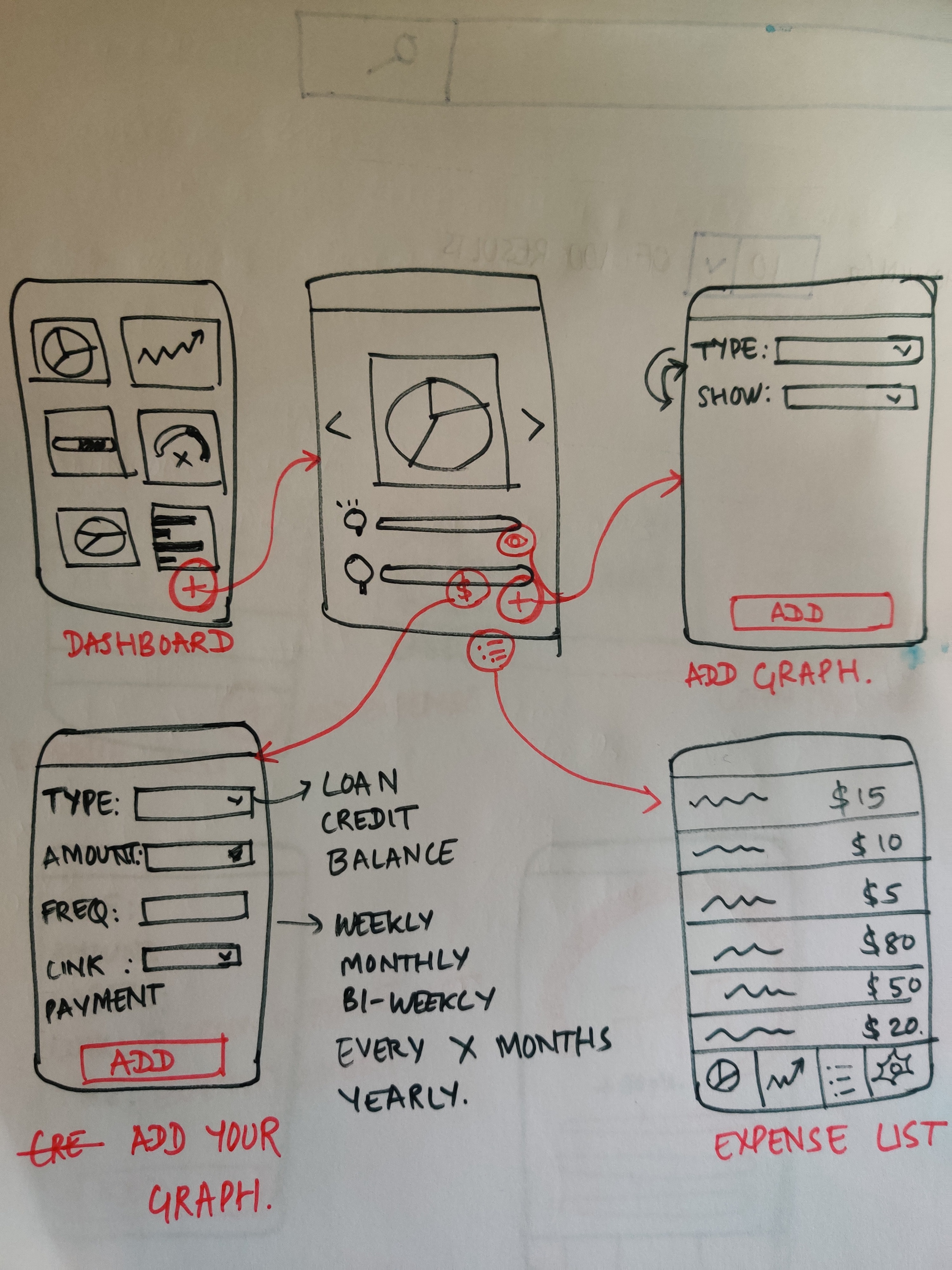

As part of the ideation process, I started storyboarding with my participants on what the user journey would look like. The idea was to see how the feedback and data we had so far, could manifest in an app.

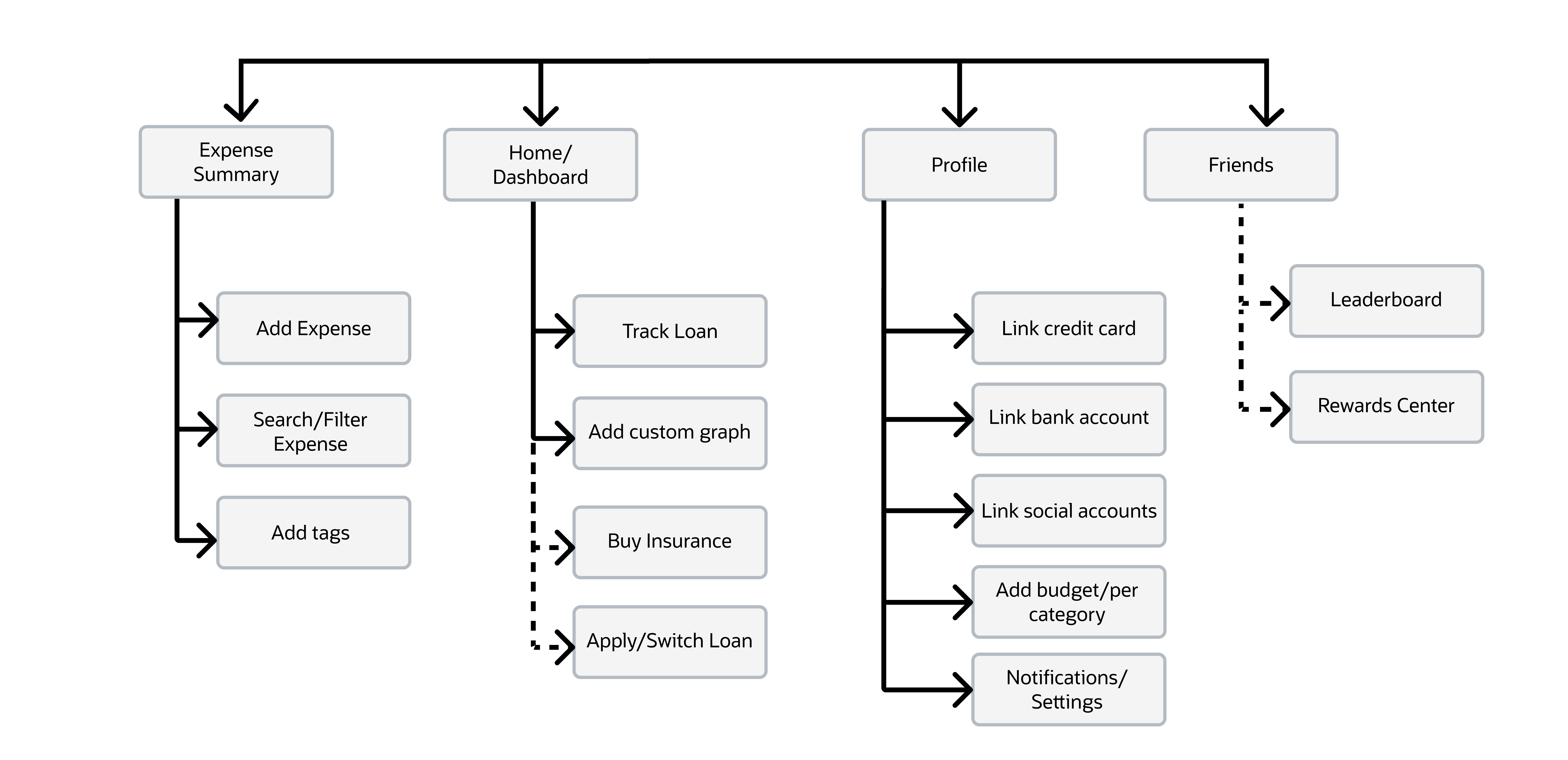

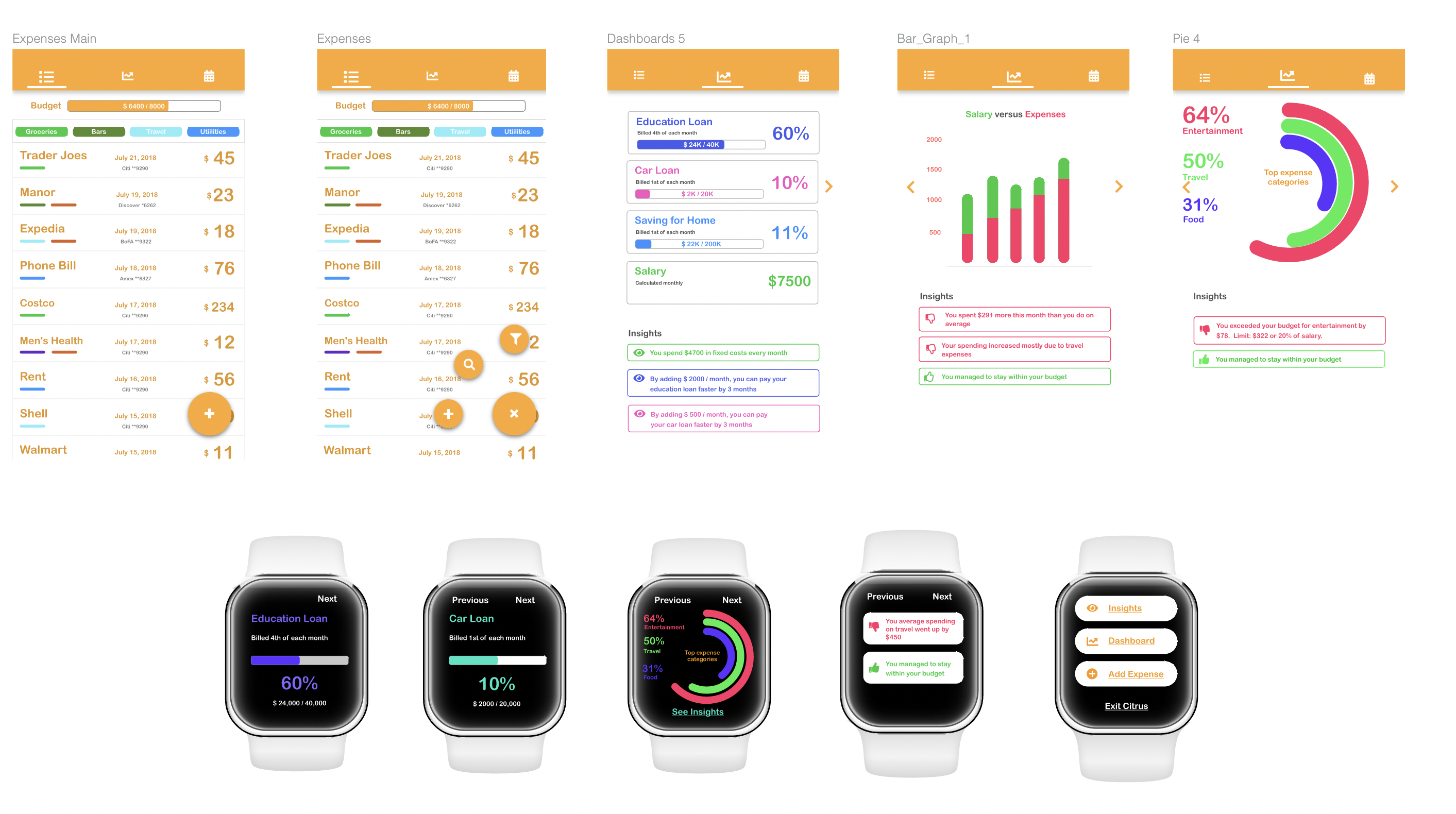

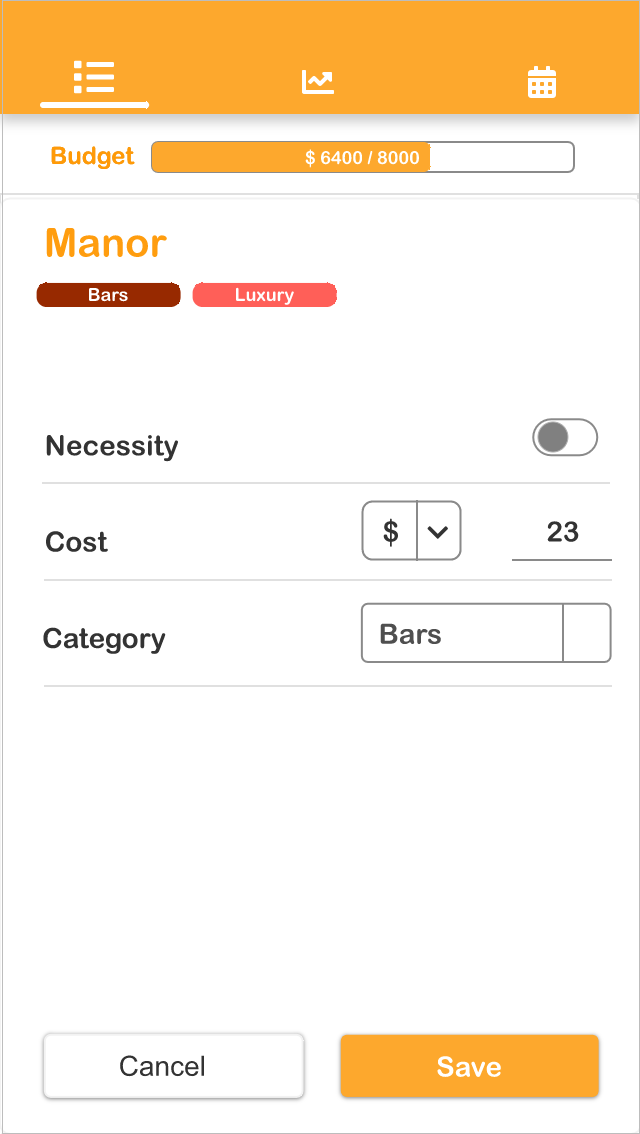

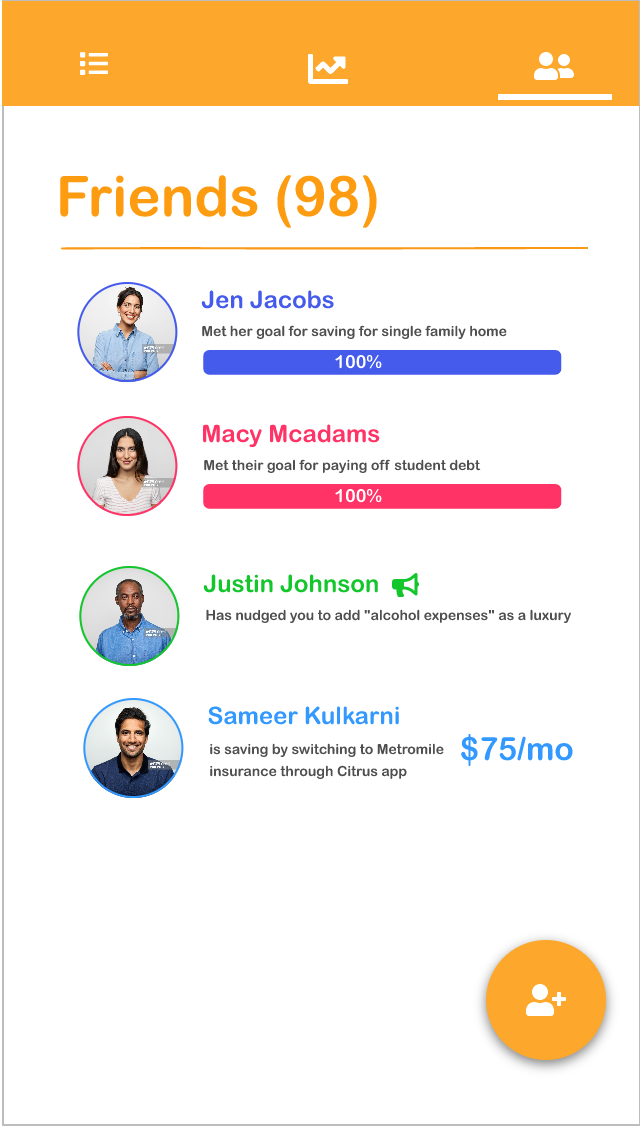

After we had visualized some ideas, the next step was to translate the low-fidelity storyboard into a concreate application pathway. After hours of brainstroming, sketching and noodling with a group of participants, we all agreed this is how the pathways should be designed.

I tested the concept and the prototype with 6 new participants, also consumers of the client's product. The participants were asked to try out the prototype, and then asked to comment on their experience. Here are some common themes I observed -

About the concept -

About the design -